Most people spend their working years focused on one thing: growing their money.

But as retirement gets closer, the question changes.

It stops being:

“How much can I grow this?”

And becomes:

“How much reliable income can this actually provide?”

That shift is why more retirees are paying attention to stability, predictable income, and intentional asset positioning. Growth still matters. But in retirement, growth without an income plan can leave you exposed in ways that feel very different from the risks you carried while still earning a paycheck.

Why Retirement Changes Everything

When income from work stops, your savings have to do a different job.

They are no longer just growing for the future. They are helping fund your present.

That money may need to cover housing, utilities, groceries, healthcare, insurance, transportation, and unexpected expenses month after month, potentially for 20 to 30 years.

A large account balance can still create stress if there is no clear plan for turning it into reliable income.

This is where many retirement strategies fall short.

Accumulation without positioning is not a retirement plan. It is a starting point.

The Risk Many People Do Not See Coming

Market volatility feels different in retirement than it does during your working years.

When you are still earning income and the market drops, you may have time to wait, recover, and keep contributing.

In retirement, you may be withdrawing money at the same time the market is down.

That combination creates a specific risk called sequence-of-returns risk.

In simple terms, early losses in retirement can be more damaging than the same losses later because you may be pulling money from a declining account before it has time to recover.

This is not a reason to avoid all market exposure.

It is a reason to be intentional about which money is positioned for income and which money is positioned for growth.

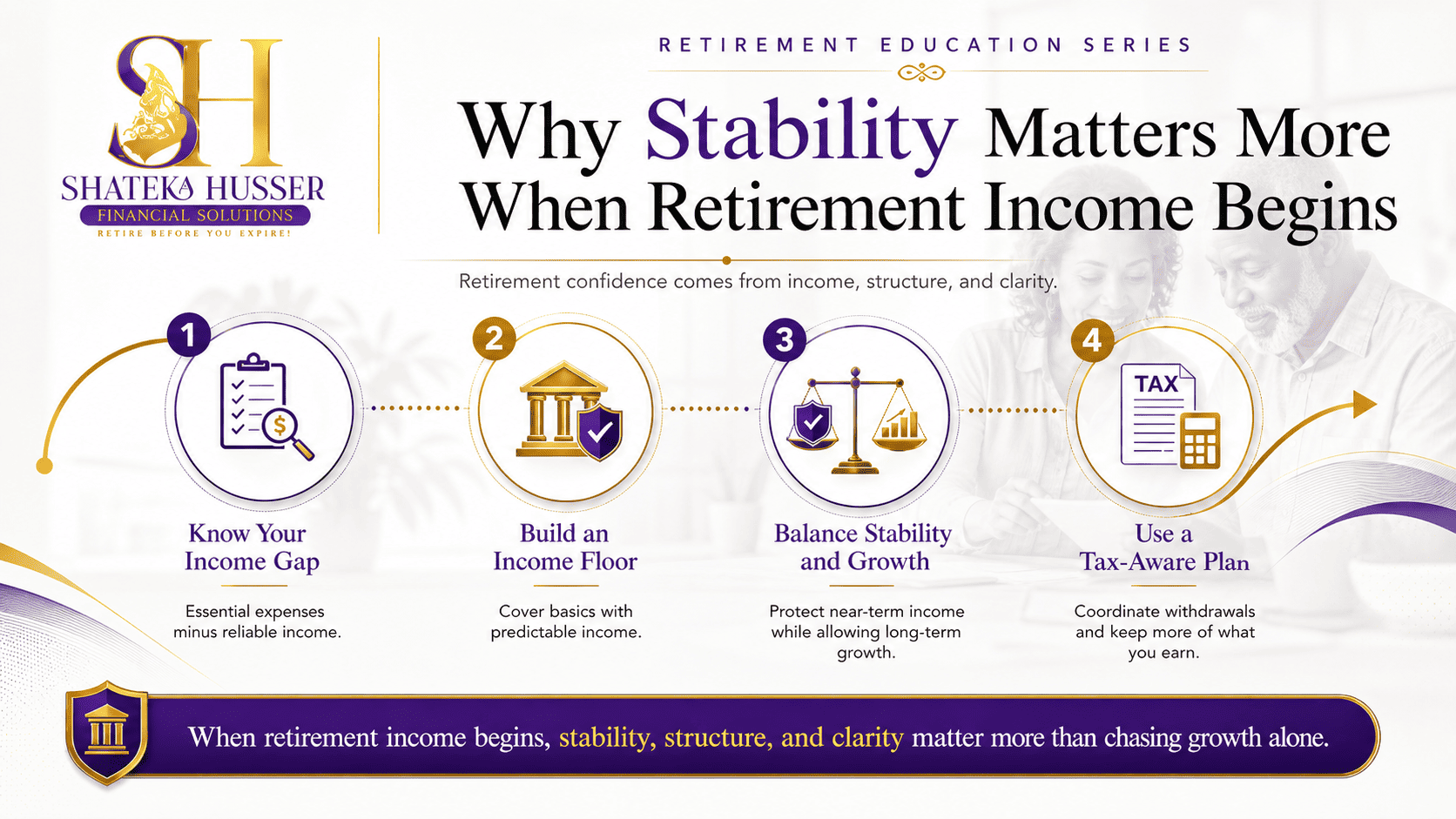

The Income Floor Framework

One practical strategy in retirement income planning is building an income floor.

The concept is simple:

Identify your essential monthly expenses, then determine how much of that is covered by reliable, predictable income.

Use this formula:

Essential Monthly Expenses minus Reliable Monthly Income equals Income Gap

For example, if your essential expenses are $4,500 per month and your reliable income is $3,200, your income gap is $1,300.

That gap is what your retirement income strategy needs to address.

Reliable income may come from Social Security, pensions, annuities, rental income, or other structured sources depending on your situation.

Once your essential expenses are covered by predictable income, your other assets may have more room to be positioned for growth, flexibility, or legacy without the same pressure of funding monthly bills.

Stability and Growth Are Not Opposites

Too much safety can create its own problems.

Inflation is real. Healthcare costs can rise. A retirement that lasts 25 or 30 years may still need growth to help maintain purchasing power over time.

The goal is not to choose all growth or all safety.

The goal is intentional balance.

Ask what role each part of your money is supposed to play:

Income: Which assets are positioned to create reliable monthly income?

Protection: Which assets are shielded from major losses, especially those needed for near-term income?

Growth: Which assets are positioned to help address inflation over time?

Liquidity: Which assets can be accessed if life changes or unexpected expenses appear?

When each dollar has a defined role, the plan has structure.

Without that structure, you are guessing.

Tax Efficiency Is Not Optional

A retirement income plan should not only ask how much income you can create.

It should ask how much income you actually get to keep.

Traditional retirement account withdrawals, Social Security, pension income, annuity income, and investment distributions may all be taxed differently.

Without a coordinated withdrawal strategy, you may create more taxable income than necessary or reduce the amount you actually get to use.

Higher taxable income may also affect certain healthcare-related costs in retirement.

The goal is not just income on paper.

The goal is spendable income.

Practical Steps to Take Now

Here are practical steps to help review whether your money is positioned for retirement income:

1. Review every account and asset you currently hold.

Look at retirement accounts, savings, investment accounts, insurance, pensions, and any other assets connected to your retirement plan.

2. Assign each asset a purpose.

Is it for income, growth, protection, liquidity, or legacy? If you cannot answer clearly, that is a starting point.

3. Separate essential expenses from lifestyle expenses.

Essentials include housing, food, healthcare, utilities, insurance, and transportation. Lifestyle expenses include travel, hobbies, gifts, and flexible spending.

4. Calculate your income gap.

Compare essential monthly expenses against reliable monthly income. The difference shows what your retirement strategy needs to solve.

5. Identify what is predictable and what is market-dependent.

Not all income sources carry the same level of certainty.

6. Reduce unnecessary risk in near-term income assets.

Money you may need soon should be reviewed differently from money meant for long-term growth.

7. Build a tax-aware withdrawal plan.

Review which accounts to use first, how withdrawals may affect taxes, and how Social Security timing, required withdrawals, and healthcare-related costs may fit into the larger picture.

8. Simplify scattered accounts when it improves clarity.

You do not always need to combine everything, but every account should have a clear role.

9. Review the plan regularly.

Taxes, expenses, health, income needs, and market conditions can change. Your plan should be reviewed before those changes create pressure.

A Quick Check

Ask yourself:

- Do I know how much monthly income my savings can realistically support?

- Do I know which portion of that income stays stable if markets decline?

- Do I have a plan for covering essential expenses without relying entirely on withdrawals?

- Have I mapped out how taxes may affect my retirement income?

- Do I know what happens if retirement lasts longer than expected?

- Is each account positioned with a clear purpose?

If most of these feel unclear, your plan may still be in the accumulation stage.

That is not a failure.

It is information.

It means the next step may not be saving more. It may be positioning what you already have.

Final Thought

Most people do not retire broke.

They retire unprepared.

Retirement should not be built on hope. It should be built with clarity around income, taxes, protection, and purpose.

When each asset has a role, when income is structured, and when the plan is reviewed regularly, retirement becomes less uncertain and more intentional.

If you are unsure whether your current strategy is truly positioned for retirement or simply invested for growth, this may be the right time to take a closer look.

Download our Retirement Ready Guide for practical insights to help you review your income, taxes, protection, and long-term stability.

Or book a Compatibility Call to review what may be worth discussing in your situation.