Most people don’t retire broke. They retire unprepared.

Unprepared does not always mean empty accounts. It can mean having money saved without a clear plan for how that money will support your life.

A balance may look strong on paper, but retirement is not lived on paper. It is lived month by month, expense by expense, and decision by decision.

The Real Problem

Saving is a habit. A retirement income plan is a strategy.

They are not the same thing.

You can contribute consistently for decades and still not know how much monthly income your accounts can realistically support. You can have solid growth and still be unsure what happens if the market drops early in retirement, expenses rise, or retirement lasts longer than expected.

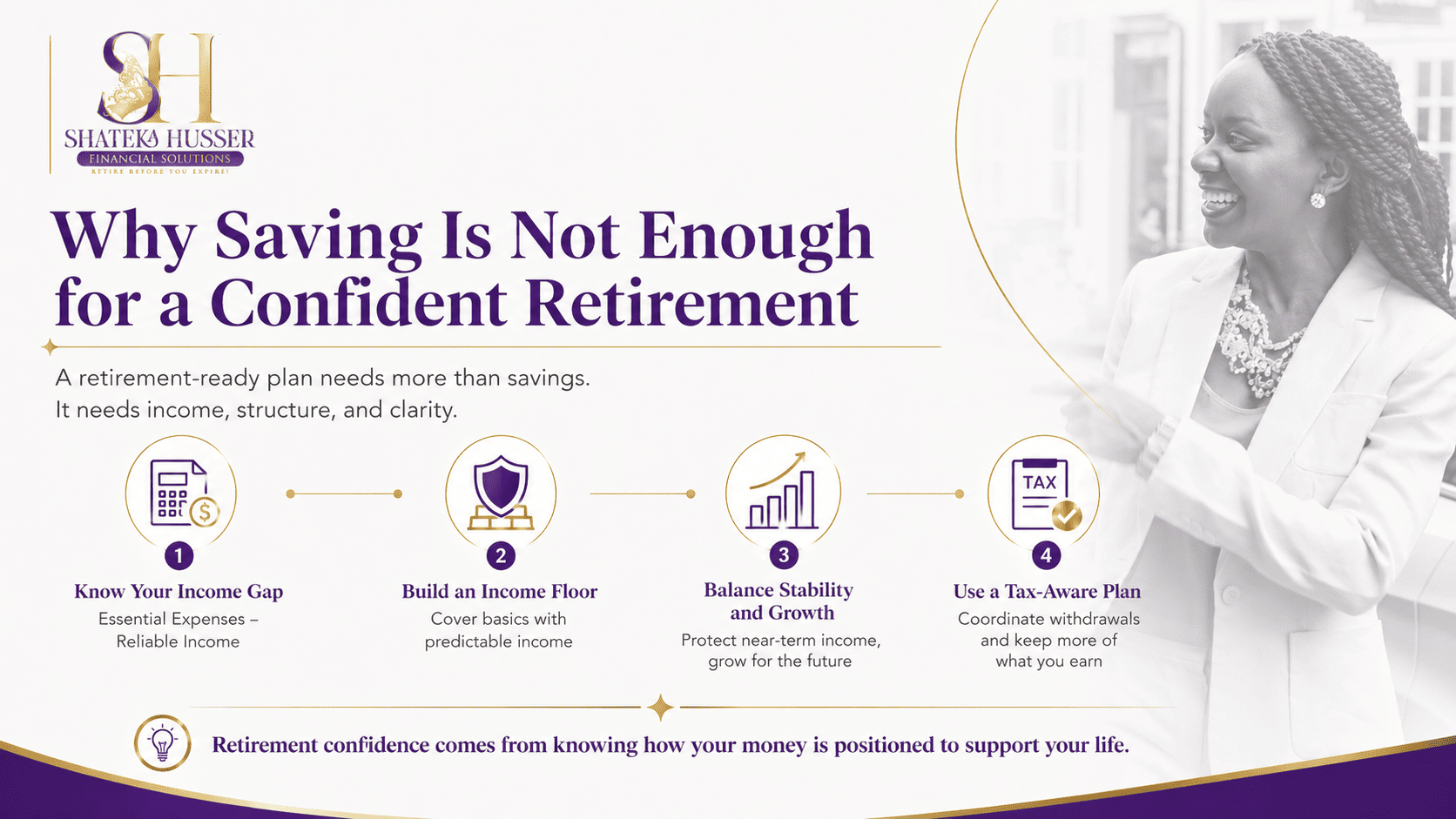

That gap between saving and knowing is where many people get stuck.

Closing that gap requires more than adding to an account. It requires positioning the money you already have with a clear purpose.

A Practical Retirement Income Framework

A stronger retirement plan should organize your money around three simple layers:

1. Income Floor

This is the income designed to cover essential monthly expenses such as housing, food, healthcare, utilities, and insurance.

It may include sources such as Social Security, pensions, annuities, or other dependable income options.

This layer is about stability.

2. Flexible Income

This is money used for lifestyle needs, unexpected expenses, and changing priorities.

It may include retirement accounts, savings, brokerage accounts, or other accessible assets.

This layer is about adaptability.

3. Regular Review

Retirement is not static. Taxes can change. Expenses can shift. Health needs can evolve. Market conditions can affect withdrawals.

This layer is about keeping the plan aligned as life changes.

Practical Steps to Take Now

Start with a simple review.

1. List every retirement account and asset you have.

Include workplace plans, IRAs, savings, investment accounts, insurance, and any other assets connected to your retirement plan.

2. Give each asset a purpose.

Ask whether each account is positioned for income, growth, protection, liquidity, or legacy. If you cannot answer that clearly, that account may need review.

3. Separate essential expenses from lifestyle expenses.

Essentials include housing, food, healthcare, utilities, transportation, insurance, and debt payments. Lifestyle expenses include travel, hobbies, gifts, entertainment, and flexible spending.

4. Calculate your income gap.

Use this simple formula:

Essential Monthly Expenses minus Reliable Monthly Income equals Income Gap

That number shows how much your savings may need to produce each month.

5. Review what is predictable and what is market-dependent.

If all income depends on withdrawals from market-based accounts, your plan may need more structure.

6. Reduce unnecessary risk before income is needed.

Money needed in the near future should be reviewed differently from money intended for long-term growth.

7. Build a tax-aware withdrawal plan.

Consider which accounts to use first, how withdrawals may affect taxes, and how Social Security timing, required withdrawals, and healthcare-related income impact may fit into the bigger picture.

8. Simplify scattered accounts when it improves clarity.

You do not always need to combine everything, but every account should have a clear role.

A Quick Readiness Check

Ask yourself:

- Do I know how much monthly income my current savings can realistically support?

- Do I know which income sources are predictable and which depend on market performance?

- If the market dropped early in retirement, could my essential expenses still be covered?

- Have I reviewed how withdrawals may affect taxes?

- Do my current accounts still match my timeline, risk comfort, and retirement goals?

- If work income stopped sooner than expected, would I know where my retirement paycheck would come from?

If several answers feel unclear, your plan may still be focused on accumulation instead of retirement income.

That does not mean you are behind.

It means this may be the right time to review how your money is positioned.

The Shift Worth Making

The better question is no longer only:

“How much have I saved?”

The better question is:

“What is this money positioned to do?”

A clear retirement income structure can help reduce uncertainty. It can show which income sources are dependable, which assets are flexible, where risk exists, and what needs to be reviewed before retirement decisions become more urgent.

You may not need to start over.

You may simply need more clarity around how your savings are positioned for income, tax efficiency, protection, and long-term stability.

Final Thought

Retirement confidence does not come from a balance alone.

It comes from knowing how that balance is designed to support your life.

If you have been saving consistently but still feel unsure about how your money will work in retirement, this may be the right time to take a closer look.

Download our Retirement Ready Guide for practical insights to help you review your income, taxes, protection, and long-term stability.

Or book a Compatibility Call to review what may be worth discussing in your situation. Clarity today creates confidence tomorrow.