And What Actually Determines Whether Your Money Lasts

You worked for decades. You saved consistently. You made sacrifices. And one day, you looked at your account statement and saw the number you had been building toward.

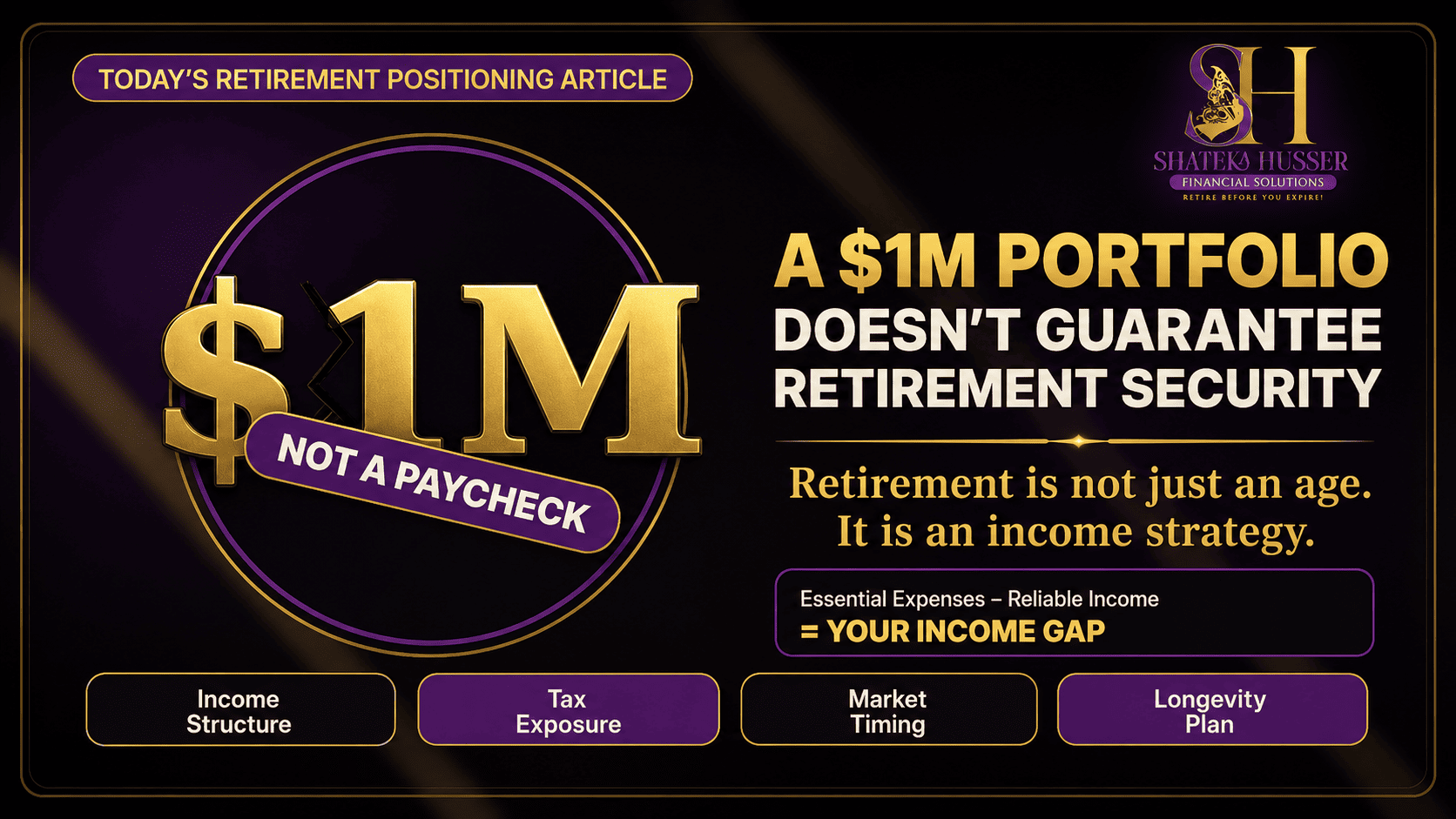

One million dollars.

By every traditional measure, you did it.

So why does retirement still feel uncertain?

If that question sounds familiar, you are not alone. Financial researchers have found that many people with significant portfolios still feel anxious about whether their money will last. Some with five million dollars feel less secure than others with far less. The difference is never just the number. It is always the structure behind it.

Most people don’t retire broke. They retire unprepared. And reaching a milestone number does not automatically mean you are prepared.

Here is what actually determines retirement security and what to review before the gap becomes a problem.

The Number Was Never the Full Answer

For decades, one million dollars was treated as the universal retirement finish line. Financial culture reinforced it. Calculators confirmed it. Conversations normalized it.

But a portfolio balance answers only one question: How much have you saved?

It does not answer:

- How much monthly income can this actually produce?

- How much will taxes reduce what you keep?

- What happens if the market drops in your first year of retirement?

- How long does this money need to last?

- Which expenses are covered by predictable income and which depend entirely on withdrawals?

Those questions determine your retirement experience. The balance is only the starting point.

The Real Gap Most People Miss

Here is where the problem becomes concrete.

A common planning assumption is the 4% withdrawal rule: withdraw 4% of your portfolio in year one and adjust for inflation each year after. On a $1 million portfolio, that is $40,000 per year, or roughly $3,333 per month before taxes.

Now consider what that actually covers in real life.

If your essential monthly expenses are $5,500 and your Social Security provides $2,200, you still need $3,300 per month from your portfolio just to cover the basics. That is before lifestyle spending, travel, healthcare surprises, or helping family.

And that is before taxes.

The formula that clarifies everything:

Essential Monthly Expenses minus Reliable Monthly Income equals Your Income Gap

That gap is what your retirement strategy needs to solve. Most people have never calculated it. Most people also feel uncertain about retirement for exactly that reason.

Why the Same Balance Produces Very Different Retirements

Consider two people who both retire at 65 with $1 million saved.

Person A has all of it in a traditional 401k. No income plan. No withdrawal strategy. Plans to figure it out as they go. Takes $70,000 in year one to cover expenses, not accounting for the fact that the full $70,000 is taxable income. Social Security not yet claimed. Market drops 18% in month three of retirement.

Person B has the same $1 million but structured differently. $400,000 in a traditional 401k, $300,000 in a Roth account, $200,000 in a taxable brokerage, and $100,000 in a cash reserve. Essential expenses are covered by a combination of Social Security and a structured income source. Portfolio withdrawals are sequenced to minimize taxes. The market drop does not force an early sell because near-term income needs are already covered.

Same balance. Completely different retirement.

The difference is not how much they saved. It is how their money was positioned.

The Four Things That Actually Determine Retirement Security

1. Income Structure

A portfolio balance is not a paycheck. Before you retire, your money needs a clear job description.

Which assets will create monthly income? Which will protect against early losses? Which will keep pace with inflation over 20 or 30 years? Which will remain accessible for emergencies?

Every dollar should have a defined role. If it does not, the plan has accumulation without strategy.

2. Tax Exposure

This is the most underestimated gap in retirement planning.

If most of your savings are in traditional retirement accounts, every dollar you withdraw is taxable income. On $1 million in a traditional IRA or 401k, your real spendable balance may be closer to $750,000 to $800,000 depending on your tax situation.

It gets more complex:

- Larger withdrawals can push you into a higher tax bracket

- Higher income can make up to 85% of your Social Security benefit taxable

- Higher income can increase Medicare premium costs

- Required minimum distributions beginning at age 73 force withdrawals whether you need the money or not, adding taxable income you did not plan for

The goal is not just retirement income. It is spendable retirement income. Planning the sequence of withdrawals, reviewing Roth conversions before required distributions begin, and balancing taxable and tax-free income sources can make a meaningful difference in what you actually keep.

3. Sequence of Returns Risk

This is the risk most people never hear about until it is too late.

During your working years, a market drop is stressful but recoverable. You are still contributing. Time is on your side.

In retirement, the math changes. If the market drops significantly in your first two to three years of retirement while you are simultaneously withdrawing income, you are pulling money from a declining account before it has a chance to recover. That combination can permanently reduce how long your money lasts, regardless of what the market does in years four through twenty.

Early retirement losses hurt more than the same losses later. This is why the money needed for near-term income should not be fully exposed to market volatility without a plan.

4. Longevity

Inflation does not create one large financial shock. It creates quiet, steady pressure year after year.

If you need $70,000 today, a 3% annual inflation rate means you will need approximately $109,000 at age 80 and $147,000 at age 90. Healthcare costs typically rise faster than general inflation, which makes this even more significant for retirees.

A retirement that lasts 25 or 30 years requires a strategy that was designed for 25 or 30 years, not just the first five.

What a Stronger Positioning Strategy Looks Like

The solution is not saving more. It is reviewing how what you already have is positioned.

Review every account and asset you hold. List your 401k, IRA, Roth accounts, brokerage accounts, life insurance cash value, pensions, and any other assets connected to your retirement. Many people are surprised to discover accounts they have not reviewed in years.

Assign each asset a purpose. Is it for income, growth, protection, liquidity, tax efficiency, or legacy? If an account has no defined role, it may not be helping your retirement the way you think it is.

Separate essential expenses from lifestyle expenses. Essential expenses include housing, food, healthcare, utilities, insurance, and transportation. These must be covered reliably regardless of what markets do. Lifestyle expenses are flexible. Treating them the same is a planning error.

Calculate your income gap. Use the formula: Essential Monthly Expenses minus Reliable Monthly Income equals Income Gap. That number tells you exactly what your strategy needs to solve.

Review which income is predictable and which depends on the market. Social Security, pensions, and certain structured income sources provide income regardless of market performance. Withdrawals from investment accounts do not. The more essential expenses you can cover with predictable income, the more stability your retirement has.

Build a tax-aware withdrawal sequence. Review which accounts to draw from first, when to claim Social Security for maximum lifetime benefit, how required minimum distributions will affect your tax picture, and whether Roth conversions before age 73 could reduce future tax pressure.

Keep liquidity accessible. A dedicated reserve for emergencies and unexpected expenses, separate from long-term retirement assets, prevents you from being forced to sell investments at the wrong time.

Review the plan regularly. A retirement strategy built five years ago may not fit your life today. Taxes change. Healthcare needs change. Expenses change. Markets change. The plan should be reviewed at least annually and whenever a major life event occurs.

A Quick Self-Review

Ask yourself these questions honestly:

- Do I know how much monthly income my current savings can realistically produce?

- Have I calculated my income gap?

- Do I know how much of my retirement income will be taxable?

- Do I understand what happens to my withdrawals if the market drops in year one of retirement?

- Is each of my accounts positioned with a specific purpose?

- Do I have essential expenses covered by predictable income sources?

- Have I reviewed Social Security timing as part of my income strategy?

- Do I have accessible liquidity separate from my retirement accounts?

- Has my retirement plan been reviewed in the last twelve months?

If most of these feel unclear, your retirement may still be positioned for accumulation rather than income. That is not a failure. It is information. And it is exactly the right time to take a closer look.

Final Thought

Reaching one million dollars is a real achievement. It represents discipline, sacrifice, and years of doing the right thing. It deserves recognition.

But the milestone is not the finish line. It is the starting point for a different and more important question: Is this money positioned to support your life?

A large balance without an income structure, a tax strategy, a withdrawal sequence, and a plan for inflation is not retirement security. It is retirement potential. Turning that potential into actual security is what retirement positioning is designed to do.

The earlier you review how your money is positioned, the more options you have to build income, reduce tax pressure, protect against risk, and prepare for the retirement you actually want to live.

Most people don’t retire broke. They retire unprepared. You still have time to make sure that is not your story.

If you are unsure whether your current strategy is truly positioned for retirement or simply invested for growth, this may be the right time to have that conversation.

download our Retirement Ready Guide or book a Compatibility Call to start creating more clarity around your retirement income, taxes, protection, and long-term stability.