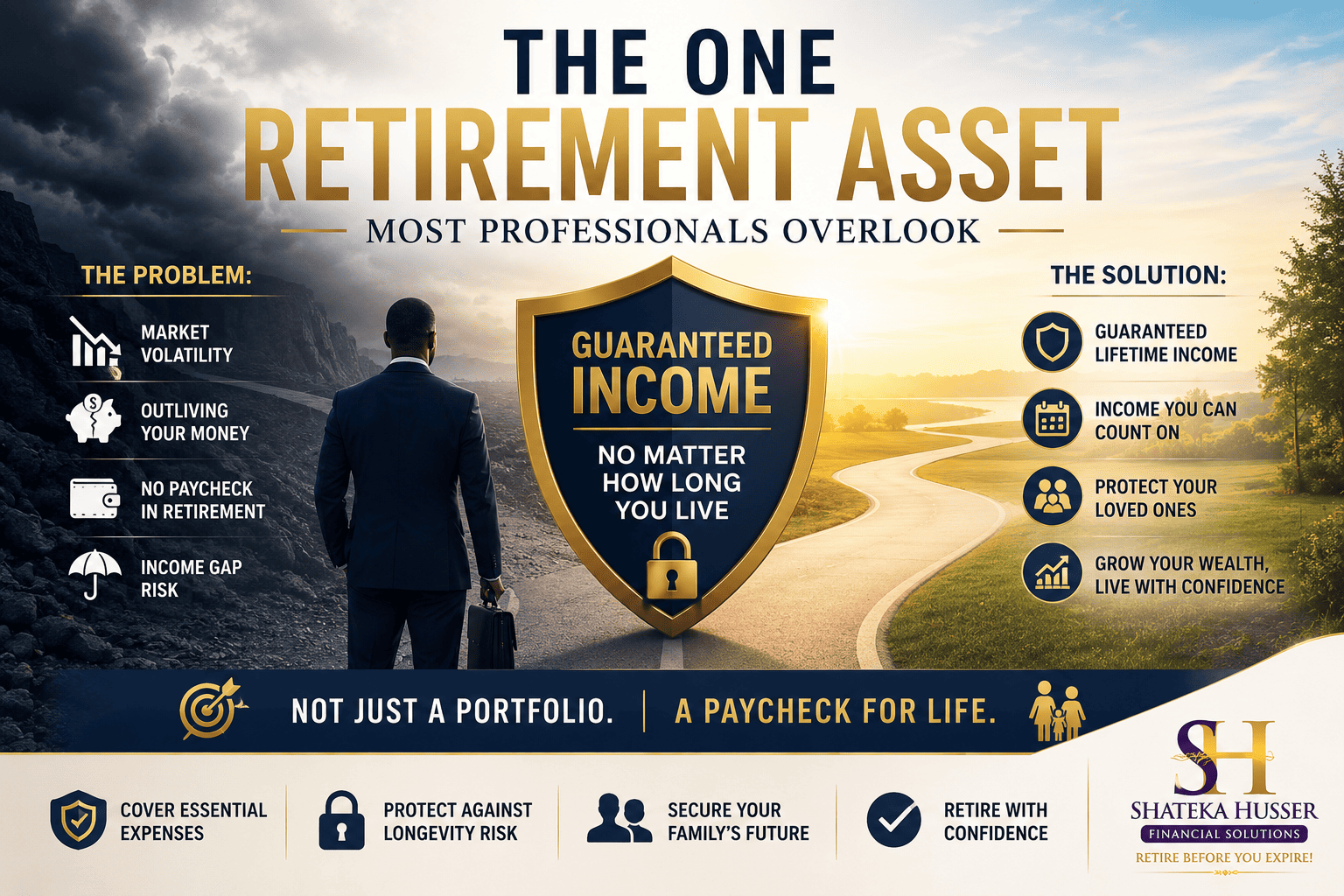

Most professionals spend decades building wealth. They contribute to retirement accounts, grow their investments, and save consistently. But when retirement arrives, many discover they solved the wrong problem. They built a portfolio. They never built an income plan.

A portfolio is designed to grow. It is not designed to pay you reliably for 25 or 30 years without running out. That is a different challenge, and it requires a different solution.

The Real Risk Nobody Talks About

The biggest financial threat in retirement is not a market crash. It is outliving your money.

The Society of Actuaries identifies longevity risk, the risk of outliving your assets, as the most underestimated threat in retirement planning today. Most retirement plans are built around the early retirement years. Very few are stress-tested for age 85, 90, or 95.

If your only guaranteed income source is Social Security, your retirement rests on a single point of support. That is a structural problem worth addressing before you need it, not after.

Why Guaranteed Income Changes Everything

Research from LIMRA Secure Retirement Institute shows that retirees with guaranteed lifetime income report significantly higher financial confidence. They spend more freely, not because they have more money, but because they know it will not run out.

That shift in confidence comes from structure, not luck.

When you have income that arrives every month regardless of market conditions, your investments no longer carry the entire weight of your lifestyle. Your portfolio can grow without being drained during downturns. Your essential expenses are covered. Your decisions become clearer.

This is what retirement income architecture looks like in practice.

What an Annuity Actually Does

An annuity is not a product for everyone. But it is the only financial tool specifically designed to solve one problem: guaranteeing income no matter how long you live.

There are several types of annuities, and they serve different purposes. Used correctly and positioned at the right time, an annuity can:

- Create a guaranteed monthly income floor that covers essential expenses

- Remove the pressure of depending entirely on market performance for living costs

- Restore the paycheck structure that retirement disrupts

- Protect a surviving spouse from a sudden income gap

- Allow the rest of your portfolio to stay invested for growth

The Right Time to Act

The 5 to 10 years before retirement are the most consequential window for income positioning. Decisions made in this period have an outsized impact on lifetime income outcomes. Waiting until retirement is already underway narrows your options.

If you have not had a specific conversation about your guaranteed income floor, now is the right time to have it.

Questions to Ask About Your Retirement Income

Use these as a starting point to review how your income is currently structured:

- What income arrives each month regardless of what the market does?

- If the answer is only Social Security, what is your plan for essential expenses beyond that?

- Have you modeled your income needs at age 85, 90, and 95?

- Does your current plan separate essential expenses from discretionary spending?

- What happens to household income if your spouse passes first?

- Are you in the optimal window to add a guaranteed income layer before retirement begins?

- Do you know your income gap? Essential expenses minus reliable income equals the number your plan needs to address.

The Bottom Line

Saving money is not the same as planning retirement income. The professionals who retire with genuine confidence are not necessarily the ones who saved the most. They are the ones who structured their income to last.

A guaranteed income layer does not replace your portfolio. It works alongside it, covering what needs to be covered so the rest of your plan can do what it was designed to do.

If your current retirement plan does not clearly answer where your income comes from at age 88, that is worth reviewing now while every option is still available to you.

Ready to Review Your Retirement Income Structure?

Schedule a complimentary Wealth Clarity Call with Shateka Husser Financial Solutions. We will look at your current income sources, identify any gaps, and help you understand what a stronger retirement income architecture could look like for your specific situation.

No obligation. No pressure. Just clarity.