Most retirement conversations focus on how much you have saved.

The more important question is how that savings becomes reliable income every single month, for as long as you live.

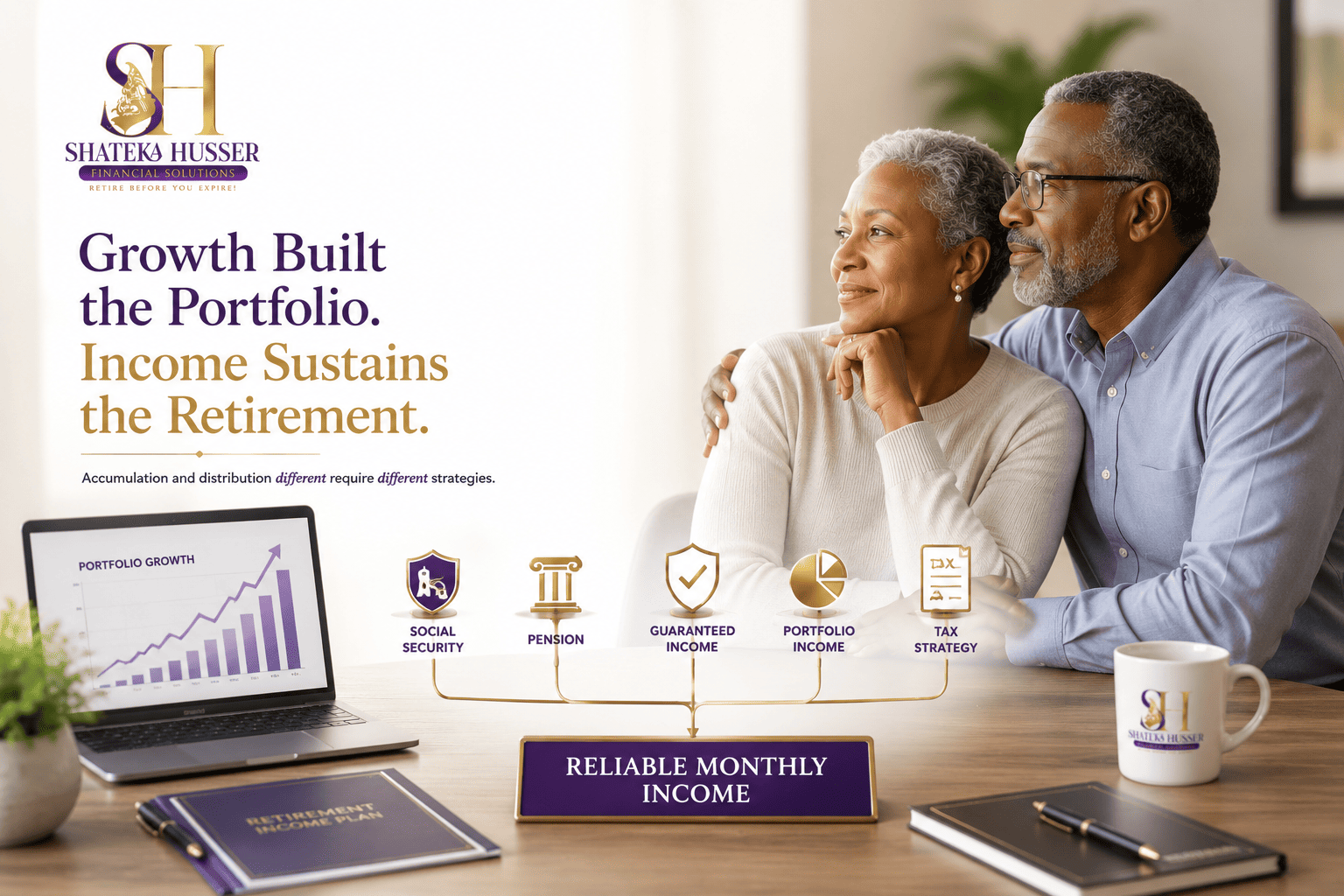

Those are two different problems, and they require two different strategies.

Building Wealth and Paying Yourself Are Not the Same Thing

The strategies that grew your money were designed to accumulate wealth. They were not designed to distribute income.

When you retire, you are no longer adding to the pile. You are drawing from it, consistently, for decades, through market cycles, healthcare expenses, inflation, and an unknown lifespan.

Without a structure built specifically for that job, your portfolio carries a burden it was never designed to handle alone.

That is why many retirees discover that having assets and having confidence are not always the same thing.

Why This Gap Shows Up Even in Strong Portfolios

Many financially successful individuals enter retirement with substantial savings and investments.

Yet research consistently shows that retirees often spend less than they can afford because they are uncertain about the future.

When every dollar of retirement income depends on a portfolio balance that changes daily, retirement can begin to feel less like freedom and more like ongoing financial management.

The concern is not necessarily running out of money tomorrow.

The concern is not knowing with certainty what income looks like ten, fifteen, or twenty years from now.

That uncertainty can quietly influence spending decisions, travel plans, gifting strategies, and overall peace of mind.

The Income Gap: What It Is and How to Find Yours

Most retirement plans contain a gap between what guaranteed income sources provide and what your lifestyle actually requires.

A simple way to identify it is:

Essential Monthly Expenses

minus

Reliable Monthly Income Sources

such as Social Security, pensions, or other guaranteed income

equals

Your Income Gap

That gap must be filled somehow.

For many retirees, the responsibility falls entirely on investment accounts.

The challenge is that investment portfolios are exposed to market fluctuations, sequence-of-returns risk, and longevity risk.

A significant market decline early in retirement can permanently affect how long a portfolio can support withdrawals.

A Practical Framework to Strengthen Your Plan

Start by evaluating what each asset is actually designed to accomplish.

Ask yourself:

- Which assets are intended for growth?

- Which provide protection?

- Which provide liquidity?

- Which support tax efficiency?

- Which create dependable income?

- Which support legacy planning?

Many people discover that the majority of their wealth is concentrated in growth-oriented assets while relatively little is positioned specifically for reliable income.

A stronger retirement plan often includes:

- Separating essential expenses from lifestyle expenses.

- Identifying which income sources are guaranteed and which rely on market performance.

- Building a tax-aware withdrawal strategy.

- Reviewing Roth conversion opportunities where appropriate.

- Stress-testing the plan against market downturns, inflation, and longevity.

- Creating a dedicated income strategy rather than relying solely on portfolio withdrawals.

Where Guaranteed Income Solutions May Fit

For some individuals, guaranteed income solutions can play an important role in closing the retirement income gap.

This is where annuities are often misunderstood.

Many people assume annuities are expensive, restrictive, or outdated. While certain products may not fit every situation, today’s annuity marketplace is significantly different than many people realize.

In fact, many of the annuity products we offer have zero fees and are available exclusively through A-rated insurance carriers.

The objective is not to replace a portfolio.

The objective is to determine whether a portion of your assets should be positioned to create predictable lifetime income that does not depend entirely on market performance.

Like any financial tool, the question is not whether annuities are good or bad.

The question is whether they fit your specific retirement goals, timeline, income needs, and overall financial strategy.

A Quick Self-Review

Take a moment to answer these questions honestly.

Can you name a guaranteed dollar amount arriving monthly at age 80—not an estimate, but a confirmed number?

If your portfolio declined by 25% during your first year of retirement, would your lifestyle change?

Does your surviving spouse maintain full income if you pass away first?

Is your retirement income strategy written down and stress-tested, or is it still a general intention?

If any of these questions give you pause, your plan may have a gap worth addressing.

Final Thought

The families who retire well are not always the ones who accumulated the most wealth.

They are often the ones who made a deliberate decision, before retirement began, to position their assets with a clear purpose:

Growth where growth is needed.

Protection where protection matters.

Tax efficiency where it creates value.

And reliable income where certainty matters most.

If you are within ten years of retirement and serious about optimizing your retirement income strategy, you may qualify for a Wealth Clarity Call.

Bring your numbers.

We will review how your assets are positioned, identify potential income gaps, and help determine whether your current strategy is designed to support the retirement lifestyle you want to achieve.

Not everyone qualifies. Qualification is based on your specific retirement planning needs and goals.