You may already have the money. The real question is whether it is positioned correctly.

Many people spend years saving and still reach retirement without a clear plan for how that money will create income, manage taxes, or hold up when markets shift. Saving builds the foundation. Positioning is what makes it work.

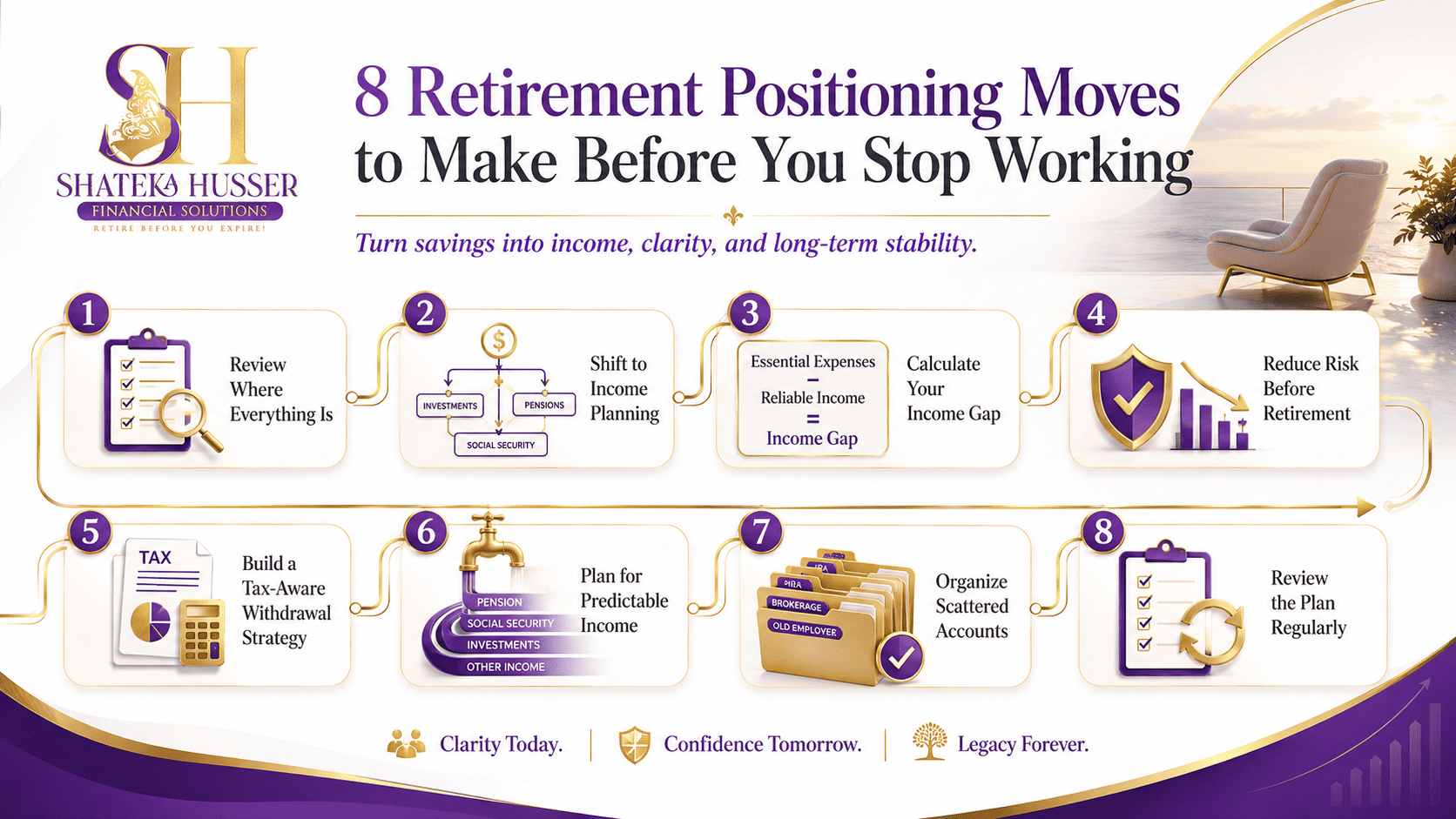

Here are eight moves worth reviewing before retirement begins.

1. Review Where Everything Is

Start by knowing what you have and where it is. Many pre-retirees have accounts spread across different stages of life that have never been reviewed together. Old workplace plans, current retirement accounts, savings, insurance policies, and investments may each be doing their own thing with no coordination.

Ask yourself:

Do I know how each account is invested?

Do I know how it will be taxed?

Do I know which ones can actually create income?

Do I know if my beneficiaries are still current?

Does each account still match my current retirement timeline?

If you cannot answer those questions clearly, that is where to start.

2. Shift From Saving to Income Planning

Saving and income planning are not the same thing. Saving builds a balance. Income planning answers what that balance will actually do once the paychecks stop.

A strong income plan addresses monthly needs, essential expenses, healthcare costs, inflation, taxes, and how long the money needs to last. Growth still matters, but growth without an income strategy does not pay the bills.

The question to ask is no longer only how much you have saved. It is how much reliable income your money can produce and for how long.

3. Calculate Your Income Gap

Before retirement begins, identify the gap between what you need and what you already have coming in reliably.

The formula is simple:

Essential Monthly Expenses minus Reliable Monthly Income equals Income Gap

Separate your expenses into two categories.

Essential expenses include housing, food, utilities, healthcare, insurance, and transportation.

Lifestyle expenses include travel, hobbies, gifts, and flexible spending.

Essential expenses should not depend entirely on market performance. That is why building an income floor matters. Once basic needs are covered by predictable income, other assets have more room to serve growth, flexibility, or legacy goals without the same pressure.

4. Reduce Risk Before You Need the Money

Risk feels different as retirement gets closer. During your working years, a market drop is stressful, but you may have time to recover. Near retirement, a market loss can be more damaging because you may be withdrawing income from a declining account at the same time.

This is called sequence-of-returns risk, and it is one reason why smart repositioning matters.

Reducing risk does not mean avoiding all growth. It means making sure the money you need soon is not carrying more risk than necessary. Review whether your current allocation still matches your timeline, not the one you had fifteen years ago.

5. Build a Tax-Aware Withdrawal Strategy

How much income you create matters. How much you keep after taxes matters more.

Different accounts are taxed differently. Traditional retirement account withdrawals, Social Security, pension income, Roth accounts, and investment income all come with different tax treatments. Without a coordinated plan, withdrawals can create unnecessary tax pressure later.

A tax-efficient strategy reviews which accounts to use first, whether Roth conversions may make sense before required withdrawals begin, how Social Security timing fits into the broader income picture, and how to spread income across account types year by year.

The goal is not just income. The goal is spendable income.

6. Plan for Predictable Income

Knowing income will continue is just as important as having money saved. Predictable income reduces pressure on market-based assets and gives retirees more confidence during volatility.

Sources of predictable income may include Social Security, pensions, rental income, annuities, or other structured income sources depending on your situation.

For some retirees, guaranteed income options are worth exploring. Certain annuities can provide lifetime income potential and help cover essential expenses without depending on market performance. They are not right for everyone and should be reviewed carefully, including fees, access, guarantees, tax treatment, and how they fit the full plan.

The goal is not to place all money into one income source. The goal is to build layers that support stability, access, growth, and flexibility.

A layered income approach often works well. One layer covers essentials. One layer supports lifestyle. One layer stays liquid for emergencies. One layer continues growing for the long term.

7. Organize Scattered Accounts

Scattered accounts create more than inconvenience. They can create duplicated risk, outdated beneficiaries, uncoordinated withdrawals, and gaps in tax strategy that are easy to miss.

Every account should have a clear purpose.

Is it for income?

Growth?

Tax efficiency?

Emergency access?

Protection?

Legacy?

If an account has no defined role, it needs a review.

Simplification does not always mean combining everything. It means making sure every account is working with the rest of the plan rather than alongside it by coincidence.

8. Review the Plan Regularly

A retirement plan that worked five years ago may not fit today. Income needs shift. Healthcare costs change. Tax rules evolve. Markets move. Family situations change.

Regular reviews help confirm that your money is still aligned with where you are now, not just where you were when the plan was created. They also help catch issues before they become expensive surprises.

The years leading into retirement are especially important. That window is often the best opportunity to reposition assets, improve tax strategy, build income clarity, and reduce unnecessary risk before it matters most.

A Quick Self-Review

Ask yourself:

Do I know how much monthly income my savings can realistically support?

Do I know which income is predictable and which depends on the market?

Have I calculated my income gap?

Do I have a tax-aware withdrawal plan?

Is each account positioned with a clear purpose?

Have I reviewed my plan in the last twelve months?

If most of these feel unclear, your money may still be positioned for accumulation rather than retirement.

That is not a failure.

It is information, and it is exactly the right time to take a closer look.

Final Thought

Most people do not retire broke.

They retire unprepared.

The earlier you review how your money is positioned, the more options you may have to build income, reduce uncertainty, and prepare for the retirement you actually want to live.

If you are ready to take a closer look, download our Retirement Ready Guide or book a Compatibility Call to start creating more clarity around your retirement income, taxes, protection, and long-term stability.