For many people, Social Security feels like a safety net they can rely on in retirement.

It is familiar.

It is consistent.

And for years, it has been positioned as something that will “be there” when work income stops.

But here is the reality most people do not fully explore until it is too late:

Social Security was never designed to carry your entire retirement.

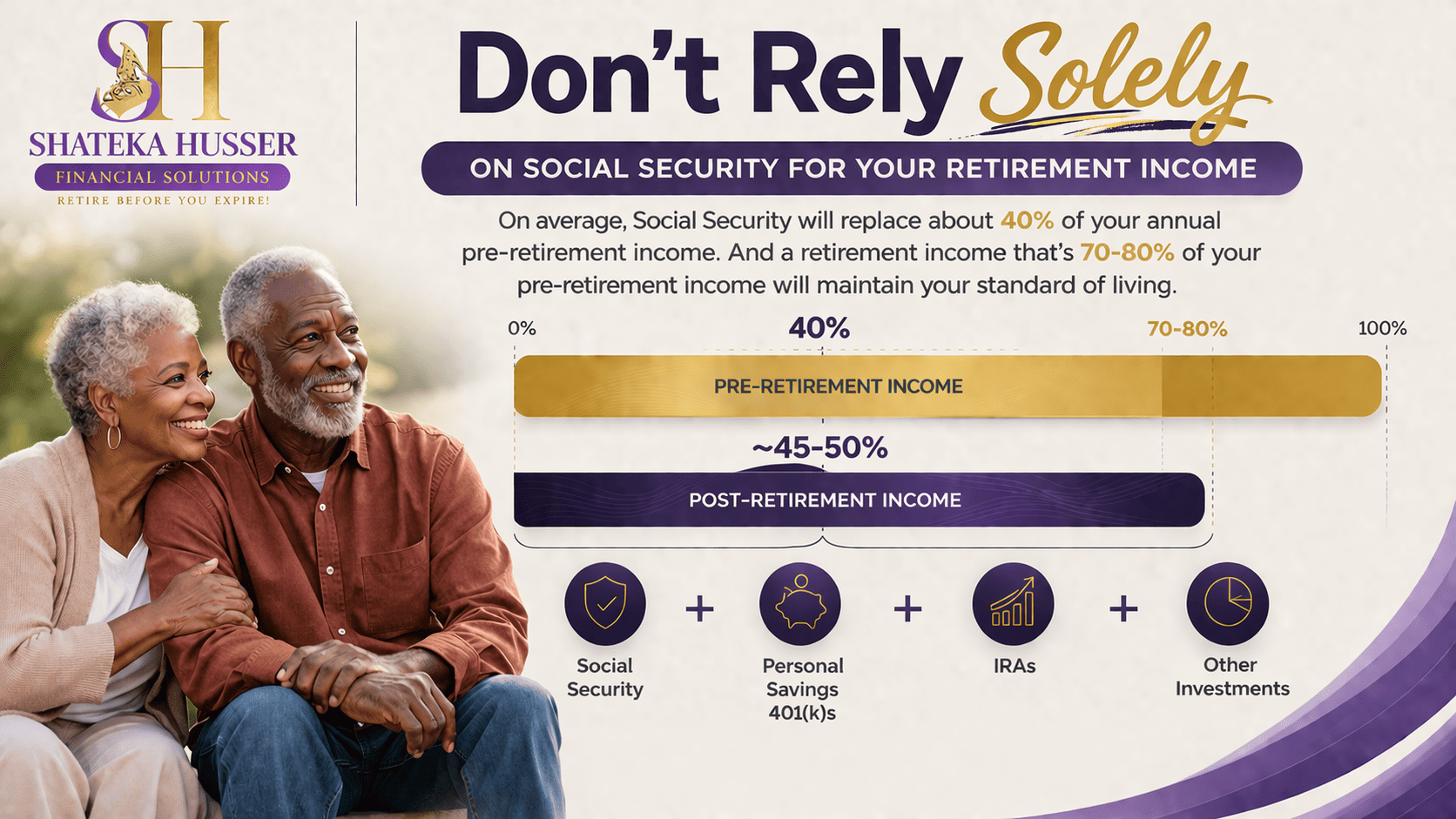

For most people, it replaces only a portion of their income, not the full amount they were earning while working. According to the Social Security Administration, it typically replaces about 40% of pre-retirement income for average earners. SOURCE

That means a gap is almost always present.

For example, if someone earned $5,000 per month while working, Social Security may provide around $2,000. The remaining $3,000 has to come from other sources.

Whether recognized early or not, that gap still exists and needs to be planned for.

Why So Many People Assume Social Security Will Be Enough

The assumption often comes from familiarity.

People contribute to Social Security for decades, so it feels natural to expect it will fully support them later. It becomes the default plan without much questioning.

But retirement today is different.

People are living longer. Costs are higher. And financial needs are more complex than they were in the past.

According to the Social Security Administration, many retirees today can expect to live well into their 80s or even 90s, meaning retirement may last 20–30 years or more.

At the same time, everyday expenses and healthcare costs continue to rise.

For example, a lifestyle that costs $4,000 per month today may require significantly more over time as prices increase, making it important for income to last longer and stretch further than many initially expect.

So while Social Security is part of the plan, relying on it alone can create a false sense of security.

What Social Security Actually Covers — And What It Doesn’t

Social Security can help cover basic income needs like housing, utilities, and essential living expenses.

But it is not designed to fully support:

- Your full lifestyle

- Rising living expenses

- Healthcare and out-of-pocket medical costs

- Unexpected financial events

That gap between what it provides and what you actually need is where many retirement plans begin to feel pressure.

Example:

If someone is used to living on $5,000 per month and Social Security provides around $2,000, there is still a $3,000 gap that must come from other sources.

That difference does not disappear.

It has to be planned for.

The Income Shortfall Most Retirees Don’t See Coming

The gap often does not feel urgent at first.

But over time, it becomes more visible.

- Prices increase.

Over time, inflation reduces purchasing power, meaning the same amount of money buys less. According to the U.S. Bureau of Labor Statistics, even moderate inflation can steadily raise the cost of everyday goods like groceries, transportation, and utilities. SOURCE - Healthcare becomes more expensive.

Medical costs tend to rise faster than general inflation. Estimates from Fidelity Investments show that a 65-year-old couple may need hundreds of thousands of dollars for healthcare in retirement, not including long-term care. - Daily living costs continue to rise.

Essential expenses such as housing, food, and insurance increase over time, making it harder for fixed income sources to keep up. This means a budget that feels manageable today may become tighter in the future as costs gradually climb.

Example

A monthly budget that feels manageable today may feel tight 10 years into retirement if expenses gradually increase while income stays the same.

This is where many people begin to feel pressure, not because they did something wrong, but because the plan was incomplete.

Why Waiting Too Long Makes the Gap Harder to Fix

Time gives you options.

When you identify a gap early, you can adjust, improve, and strengthen your strategy with more flexibility.

But when planning is delayed, choices become limited.

That is when people may have to:

- Delay retirement

Many people end up working longer because their savings and expected income are not enough to support the retirement lifestyle they want. AARP notes that working longer can increase Social Security benefits and give people more time to strengthen cash flow, which shows how often retirement timing is affected by income gaps. - Reduce their lifestyle

When income falls short, people often have to cut back on major expenses like housing, travel, and discretionary spending. The CFPB specifically suggests reducing large expenses such as housing, and AARP points to downsizing as a practical response when retirement income is tight. - Or make financial decisions under pressure

When planning is delayed, choices often have to be made quickly around claiming Social Security, adjusting spending, or covering unexpected costs. The CFPB emphasizes budgeting for rising out-of-pocket health costs, and also notes that claiming Social Security early can reduce monthly benefits by as much as 30%, which can make rushed decisions more costly. And in many cases, this situation could have been avoided with earlier clarity.

How to Build Income Beyond Social Security

A strong retirement strategy does not depend on one source of income.

It focuses on building a structure that supports your life from multiple angles.

This means understanding:

- Where your income will come from

A strong plan should clearly show which sources will support you in retirement, such as Social Security, savings, investments, pensions, or other income streams. - How long it needs to last

Your income should be planned to support not just a few years, but potentially decades of retirement, especially as people are living longer. - How rising costs will affect it

Inflation, healthcare, insurance, and everyday living expenses can reduce how far your income goes over time, so those increases should be considered early. - How to manage it over time

Retirement income should be managed carefully through different stages of life so it can adapt to changing needs, unexpected expenses, and long-term goals.

Because retirement is not just about having money.

It is about knowing how that money will support your life with stability and confidence.

Next Step

If you are unsure how Social Security fits into your overall plan, this is the time to take a closer look.

The goal is not just to retire.

The goal is to retire with clarity, confidence, and a plan built for real life.

👉 Book a compatibility call to get clear on your next steps.