Having a larger retirement income is great; having a larger tax-free retirement income is even better.

Here are six ways you may be able to earn tax-free income in retirement.

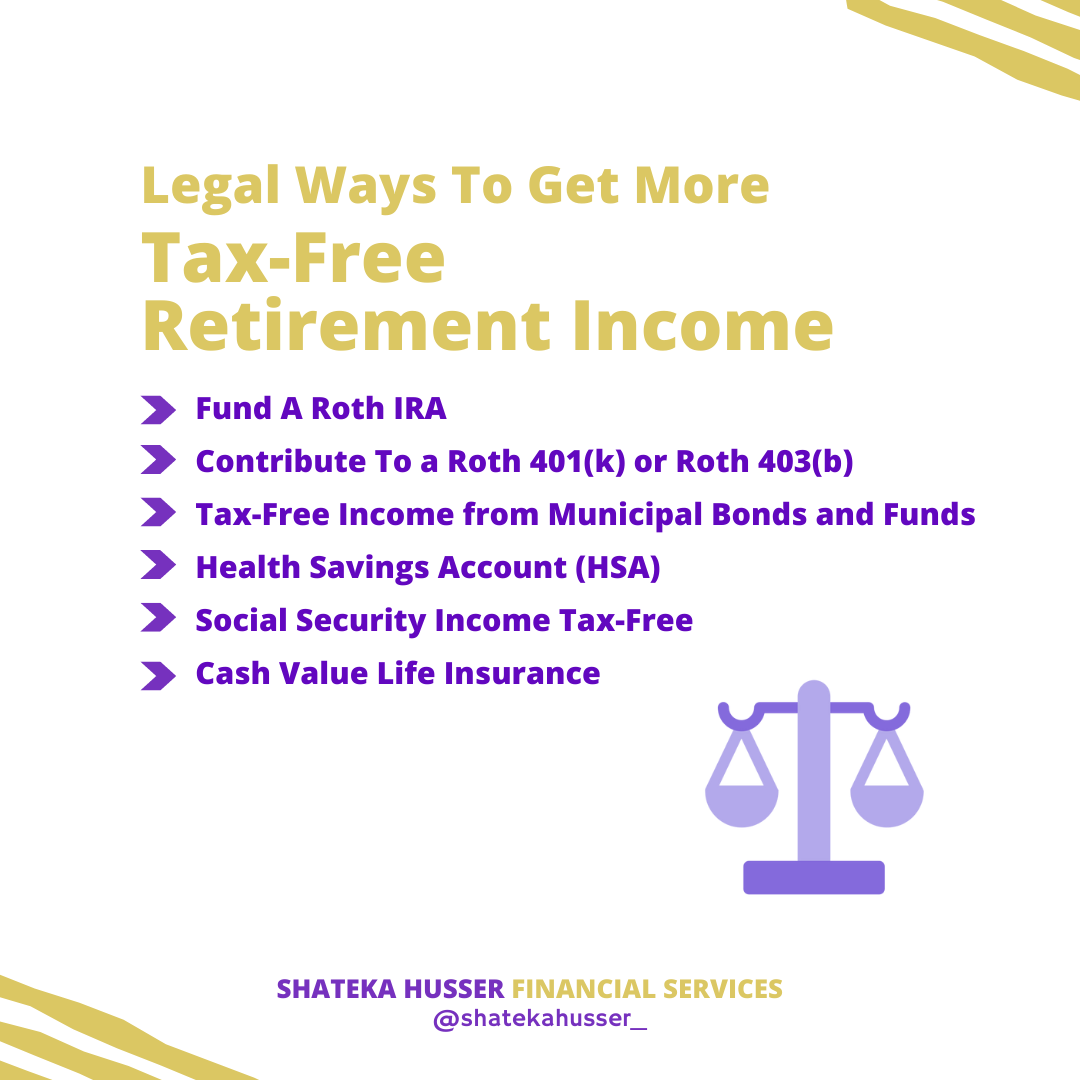

Fund A Roth IRA

Think of the Roth IRA as the starter account for tax-free income in retirement. In 2022, you can contribute $6,000 to your Roth IRA ($7,000 if you are 50 or older). There is no tax deduction for your Roth IRA contributions, but the money grows tax-free, and, most importantly, the money comes out as tax-free income during retirement.

Contribute To a Roth 401(k) or Roth 403(b)

Using the Roth option, your 401(k) or 403(b) can be a great way to build tax-free retirement income, assuming your retirement plan allows for Roth contributions. Similar to Roth IRA contributions, your growth and withdrawals within your Roth 401(k) are tax-free. The difference is that you have the ability to contribute up to $20,500 in 2022, as well as a $6,500 catch-up if you are 50 years of age or older.

Tax-Free Income from Municipal Bonds and Funds

Buying municipal bonds (either individually or via funds) is the most investment-specific of the tax-free income options. Income distributions from municipal bonds are not subject to federal income taxation, but they may still be subject to state income taxes. For this reason, the interest rates municipal bonds pay is generally lower than that of taxable bonds.

Health Savings Account (HSA)

Investing for retirement via an HSA is the triple whammy of tax-free income. You can get a tax deduction for contributions, the growth, and, if taken properly, withdrawals from an HSA are also tax-free. You will need to have the appropriate type of health insurance plan to open and fund an HSA. This account is meant to be used to pay for current medical expenses, but you don’t have to pay for them now. You could hold the HSA until retirement with the assets growing and compounding along the way. You could then reimburse yourself for all the medical expenses you paid over the years (make sure to keep your receipts). Expenses can include Medicare premiums.

Social Security Income Tax-Free

If your taxable retirement income is small enough, you can receive your Social Security benefits tax-free. I am going to go out on a limb here and say unless you have substantial tax-free income here, you do want to be taxed on your Social Security. The reason is that if your total income is low enough for your Social Security to not be taxable, you are likely sitting near the poverty line.

In 2022, at an income of just $25,000 (single) or $32,000 (married), your Social Security benefits begin to be taxed. Keep in mind this includes your Social Security checks as well as all other taxable retirement income.

Cash Value Life Insurance

You should think of life insurance as an asset class for your retirement and tax planning. Essentially, you can set up this account like a Roth IRA without income or contribution limits. You won’t get a tax deduction for your premiums, but the money will grow tax-free. If handled properly, it will come out tax-free. Also, these accounts won’t incur IRS penalties for withdrawals before you reach 59 ½. This can be a huge bonus for people looking to reach financial independence and retire early (pre 59.5).

Please let me know if you have any questions. I’m here to help! To your incredible FINANCIAL success! “RETIRE BEFORE YOU EXPIRE”

– SHATEKA Husser